AI driven insurance underwriting is no longer just hype it’s hitting prime time with serious institutional backing. On March 3, 2026, Boston based Gradient AI landed growth capital from CIBC Innovation Banking, a powerhouse lender that has fueled over 700 tech companies in recent years. This isn’t seed money for unproven ideas; it’s fuel for scaling proven tech in a maturing market. With CIBC managing over $11 billion in funds, their vote of confidence signals insurtech’s shift from experimental to essential.

What Gradient AI Brings to the Table

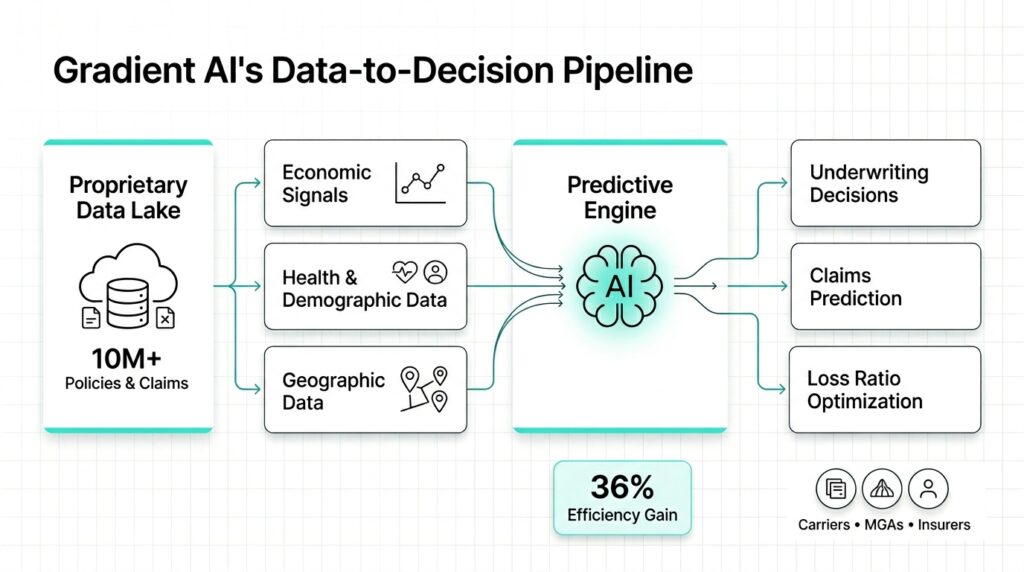

Gradient AI sits at the crossroads of massive data and real world insurance risks. Their SaaS platform taps into a proprietary data lake covering tens of millions of policies and claims, enriched with economic trends, health stats, geographic patterns, and demographic insights. This powers predictive tools that help insurers tighten loss ratios, accelerate quote approvals, and slash claims costs through smart automation.

Clients include big carriers, managing general agents (MGAs), managing general underwriters (MGUs), third party admins, risk pools, and self insured giants across property, casualty, life, health, and more. CEO Stan Smith emphasized the funding’s impact: “We’re thrilled with CIBC’s support, but now it’s on us to tackle industry pain points by supercharging our platform and delivering top-tier value.”

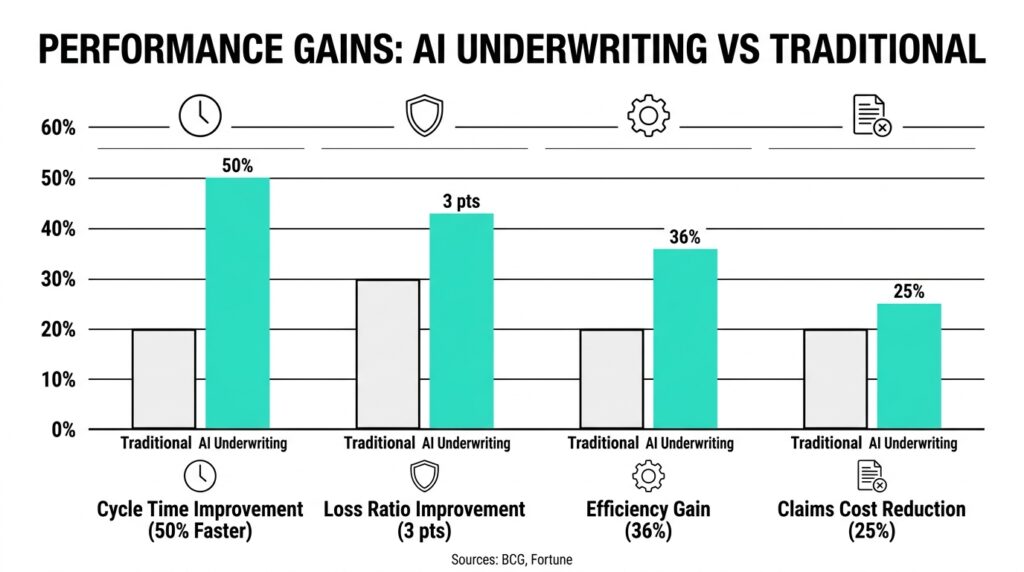

Smith highlights how insurers are getting savvier at risk assessment, yet manual processes drag them down. Gradient AI automates these, cuts expenses, and boosts outcomes think faster decisions without the guesswork. According to McKinsey’s 2025 Insurtech Report, platforms like this can reduce underwriting cycle times by 40-50% by integrating alternative data sources, such as telematics for auto insurance or wearable health data for life policies.

A Booming Market Hungry for AI Innovation

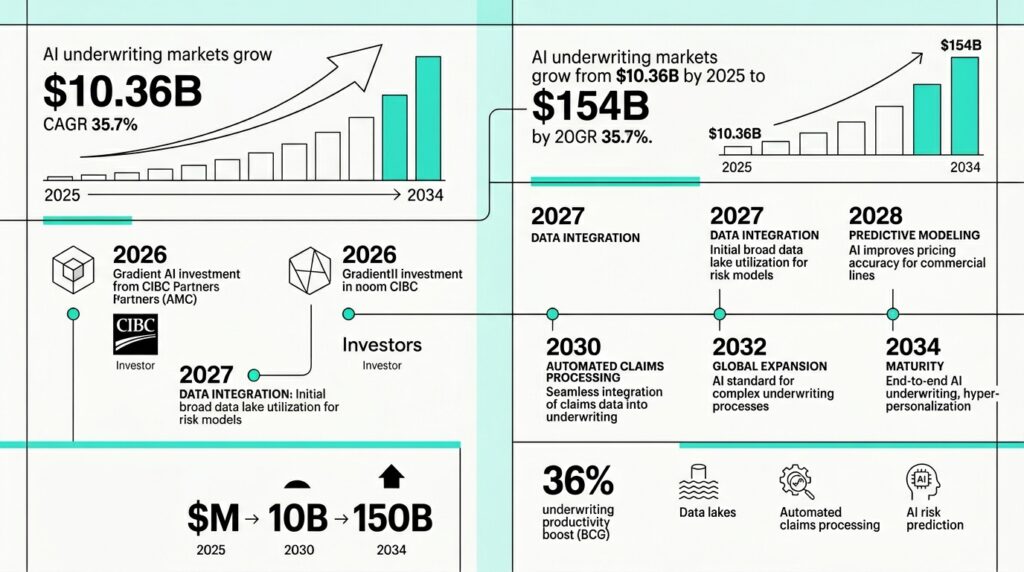

The timing couldn’t be better. The global AI in insurance market hit $10.36 billion in 2025 and is on track for $13.45 billion in 2026, racing toward $154 billion by 2034 at a 35.7% CAGR, per Fortune Business Insights. Deloitte’s 2025 Insurance Outlook adds that 68% of insurers plan to double AI investments this year, driven by rising claims from climate events and cyber threats.

BCG research shows AI can boost complex underwriting efficiency by 36%, especially by handling unstructured data like emails or images potentially trimming loss ratios by 3 points. For context, traditional underwriting relies on static actuarial tables, but AI layers in dynamic signals like real-time weather for property risks or social determinants for health claims.

Take property and casualty lines: Statista reports AI could save the industry $40 billion annually by 2030 through fraud detection alone. Gradient AI’s tools exemplify this, predicting claims with 20-30% higher accuracy than legacy models, based on similar platforms analyzed in PwC’s AI in Financial Services study.

Navigating Regulations and Gaining an Edge

Adoption pressure isn’t just from rivals regulators are demanding transparency. In the US, the NAIC’s AI guidelines push for explainable models, while Europe’s AI Act classifies insurance AI as “high-risk,” requiring audit trails. Gradient AI’s setup shines here: its core engine uses contextual layers for traceable predictions, making compliance easier.

George Bixby, Director at CIBC Innovation Banking, nailed it: “Gradient AI’s AI approach is transforming risk assessment, claims handling, and customer value.” This aligns with Gartner’s 2026 forecast that explainable AI (XAI) will be mandatory for 75% of regulated industries by 2028, giving early adopters like Gradient a head start.

Real world wins? Early adopters report 25% drops in manual reviews, per a 2025 Celent survey of 200 insurers. For self insured employers, this means billions saved on workers’ comp claims by flagging high risk profiles pre-hire.

Gradient AI’s Stellar Investor Lineup

Gradient isn’t new to backers. They boast Centana Growth Partners, MassMutual Ventures, Sandbox Insurtech Ventures, and Forte Ventures. MassMutual Ventures stands out it’s the VC arm of one of America’s largest mutual life insurers, proving the tech’s street cred from the very industry it disrupts.

CIBC’s growth capital flips the script from equity rounds to execution mode. It’s a sign: AI underwriting isn’t tweaking spreadsheets; it’s rebuilding how insurers price the unpredictable, from pandemics to cyber breaches.

Why Insurers Can’t Afford to Wait

For laggards treating AI as a side project, the train is leaving the station. McKinsey notes top performers using AI see 15-20% higher premiums from precise pricing, while laggards leak margins. Emerging trends amplify this: agentic AI (autonomous agents) could automate 50% of underwriting by 2028, per BCG, handling end to end workflows.

Challenges remain data privacy under GDPR/CCPA, model bias mitigation but Gradient AI’s audited, scalable platform addresses them head on. As climate risks surge (claims up 30% YoY per Swiss Re), AI’s predictive power becomes non negotiable.

Looking ahead, integrations with IoT (e.g., smart home sensors) and generative AI for personalized policies will redefine the game. Gradient AI, with fresh capital, is positioned to lead, turning underwriting from art to science.

In summary, Gradient AI’s funding marks insurtech’s inflection point. Insurers ignoring this risk obsolescence; adopters gain a competitive moat. What’s your take on AI’s role in your industry?

Check out more on our blog page now → AI, Tech, Cybersecurity