China’s brain computer interface (BCI) sector is surging past research labs into real world applications, outpacing many global rivals. Startups are scaling implantable and noninvasive tech with government backing and investor cash, eyeing everything from medical treatments to human enhancement.

Key Growth Drivers

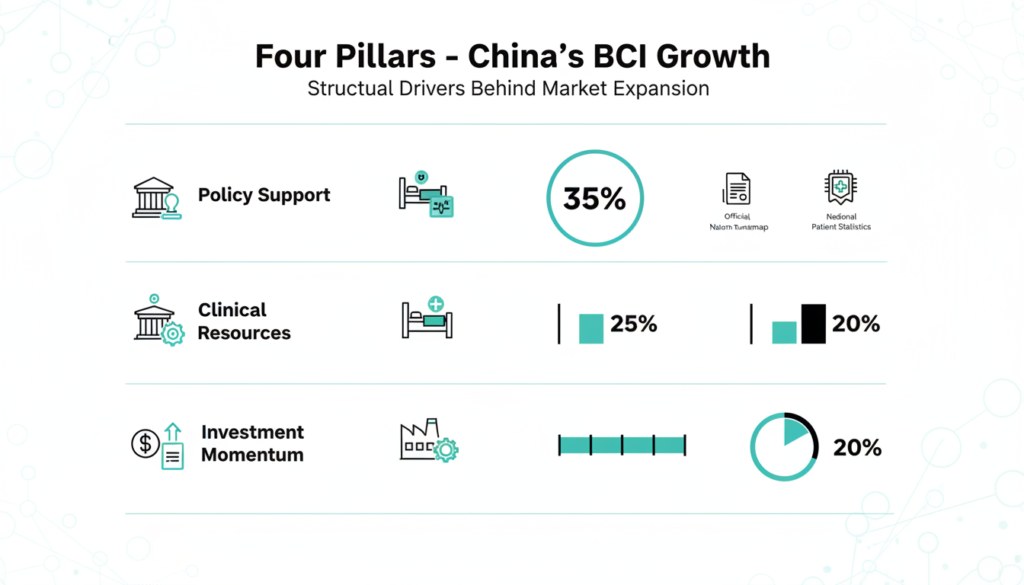

Phoenix Peng, who leads noninvasive BCI firm Gestala and co founded implant maker NeuroXess, credits four main forces. Strong policies from provinces like Sichuan, Hubei, and Zhejiang set BCI medical pricing, paving the way for national insurance coverage. This speeds up adoption compared to slower U.S. insurer approvals.

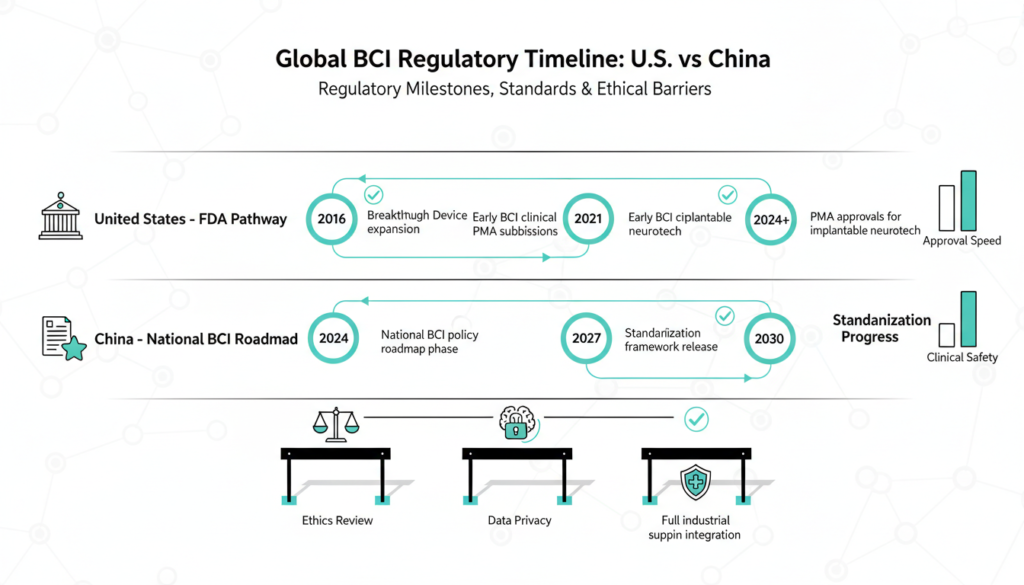

In August 2025, China’s industry ministry unveiled a roadmap targeting 2027 tech breakthroughs, standards by then, and a full supply chain by 2030. At the 2025 Shenzhen BCI Expo, officials launched an 11.6 billion yuan ($165 million) brain science fund. This supports firms from lab work to market launch.

Peng predicts healthcare dominance in 3 5 years, with multibillion-dollar scale as insurance expands.

Clinical Trials Lead the Way

China boasts huge patient pools and low trial costs, accelerating progress. Researchers finished the nation’s first fully implanted wireless BCI trial only the second worldwide after Neuralink’s letting a paralyzed patient control devices sans wires.

By mid 2025, over 50 flexible implant trials advanced motor decoding, language, spinal repair, and stroke rehab. Next up: whole brain decoding with ultrasound like Gestala’s. Peng notes traditional electrical BCIs paved the way, but innovations now target broader neural encoding.

National health insurance fast tracks approved devices to patients, unlike fragmented U.S. systems.

Top Startups in Action

Key players include NeuroXess (implants), Neuracle, NeuralMatrix, BrainCo (noninvasive and limbs), Bo Rui Kang Tech, Aoyi Tech, Brainland Tech, and Zhiran Medical. Shanghai’s StairMed grabbed $48 million in Series B funding in February 2025. BrainCo filed for a Hong Kong IPO after raising $287 million.

Gestala, launched January 2026, eyes angel funding and Q3 product rollout. Early trials cut chronic pain by 50% per session, lasting 1-2 weeks ideal for stroke, depression.

BCI Types Explained

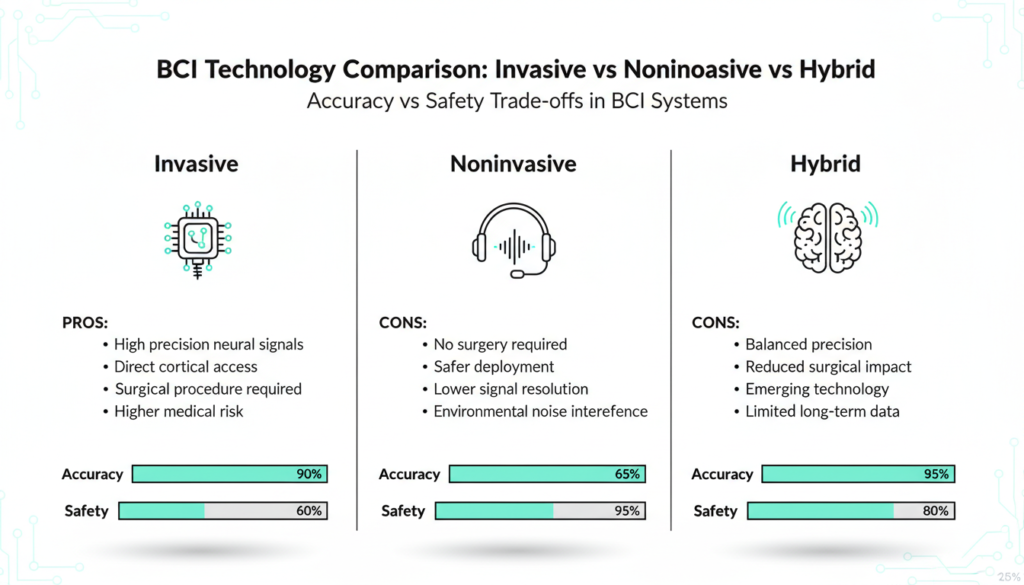

Invasive BCIs like NeuroXess or Neuralink embed electrodes for neuron level precision but require surgery risks. Noninvasive options from NeuroSky or BrainCo use EEG headsets reading skull signals safer, easier, less precise.

Emerging hybrids blend ultrasound, magnetoencephalography, magnetic stimulation, and optics. These boost safety and scalability, dodging surgery fears. Ultrasound targets pain and neuro conditions with patient buy in.

Investment and Manufacturing Edge

China’s semiconductor, AI, and med tech factories enable rapid prototypes. State funds and VCs pour in via national drives. HSG (ex-Sequoia China) backs Zhiran Medical’s anti inflammatory flexible electrodes, tackling rigid implant issues like signal fade.

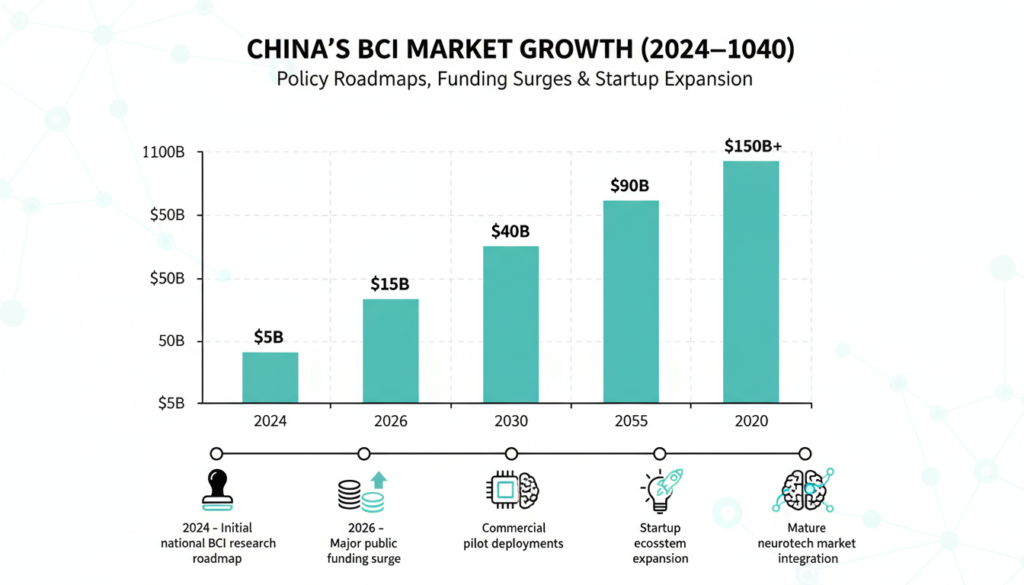

HSG’s Yang Yunxia stresses viability over hype lowering costs, clearing barriers for sustainable biz. Market hit $530 million in 2025 (from $440 million in 2024), projected at 120 billion yuan by 2040.

Future Regulations and Ethics

Over five years, rules will sync with IEC, ISO, and FDA standards, prioritizing data privacy and approvals. Invasive devices face stricter checks; noninvasive get easier paths. Ethics ramp up consent, expand reviews beyond medicine, and standardize trials.

BCIs promise “high bandwidth” brain AI links, merging carbon and silicon smarts. Peng sees neuroscience AI fusion as inevitable, unlocking vast markets beyond health like augmentation.

Global BCI Landscape

China’s BCI momentum challenges U.S. dominance, with Neuralink, Synchron, and Paradromics facing stiff competition. The global BCI market is projected to reach $3.5 billion by 2030, fueled by neurorehabilitation, gaming, and cognitive enhancement demands. While U.S. firms excel in high precision invasives, China’s volume in clinical trials and manufacturing scale offers faster iteration.

European players like CorTec (Germany) focus on hybrid implants, but lag in commercialization. Noninvasive leaders include Emotiv (Singapore based, U.S. market focus) with consumer EEG headsets for meditation apps. Adoption barriers persist: invasives limited to ~1,000 patients worldwide due to risks; noninvasives hit consumer markets but struggle with signal noise.

Technical Innovations Breakdown

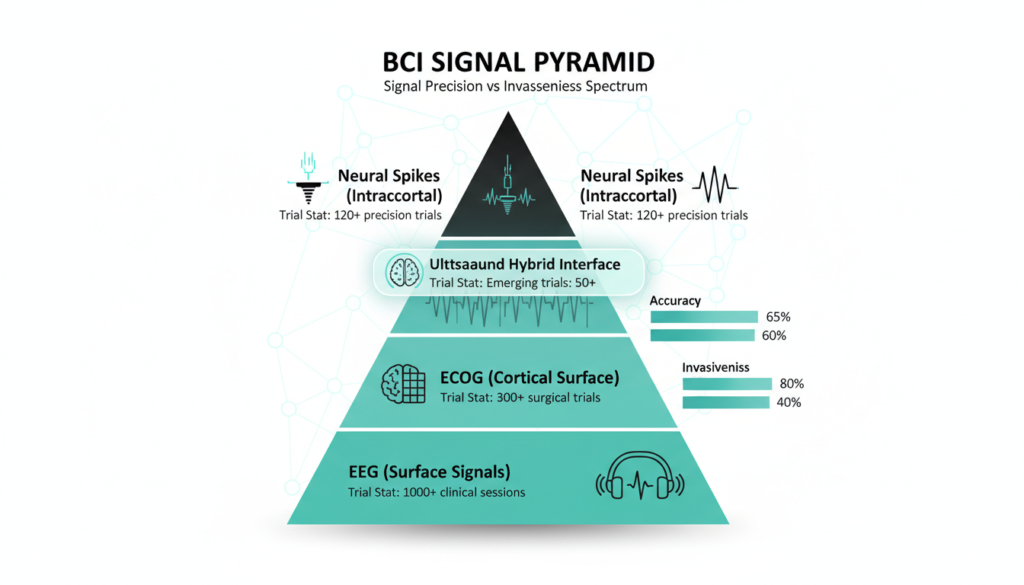

BCIs capture signals differently: EEG (scalp electrodes, noninvasive, 1-100 Hz), ECoG (surface brain grids, semi-invasive), intracortical arrays (Utah style, neuron spikes up to 1,000 channels). China’s flexible electrode cuffs from Zhiran Medical reduce gliosis (scarring), claiming 6 month stability vs. 3 for rigid Neuralink threads.

Gestala’s ultrasound (fUS-BCI) penetrates skull for deep focus without surgery, modulating pain circuits in thalamus early data shows 50% relief lasting weeks. AI decoders use transformers for 90% motor intent accuracy; closed loop systems now encode stimuli back to brain, restoring vision in trials.

By 2027, China’s roadmap eyes 1,000+ electrode arrays matching Blackrock’s Utah system, integrated with LLMs for natural language BCIs.

Investment Trends for U.S. Investors

VC flows heavily U.S. bound ($2B+ in 2025), but China’s state backed $165M fund and deals like StairMed’s $48M draw attention. BrainCo’s HK IPO filing signals maturity. U.S. parallels: Precision Neuroscience raised $41M; Paradromics $33M for speech decoding.

Risks loom: FDA scrutiny slows trials (Neuralink’s PRIME study hit delays); private insurers balk at reimbursement. China bypasses via national insurance. For U.S. portfolios, bet on noninvasives like ultrasound lower barriers, scalability for depression/stroke markets ($100B+ TAM).

| Company | Type | Funding (Recent) | Key Milestone |

|---|---|---|---|

| Neuralink | Invasive | $680M total | Human implants 2024 |

| Synchron | Stent-based | $145M | FDA breakthrough 2025 |

| StairMed | Invasive | $48M Series B | China trials scaling |

| Gestala | Ultrasound | Angel round | Pain relief 50% trials |

| Paradromics | Invasive | $88M total | 500+ channels planned |

Regulatory and Ethical Hurdles

U.S. FDA classifies BCIs as Class III devices, requiring PMA trials costing $50M+. China aligns with IEC/ISO for standards, easing noninvasive paths while tightening invasives. Data ethics critical: brain signals as “neuro-rights” under debate U.S. states eye laws mirroring EU AI Act.

Challenges: 20% annual signal drift, 5% infection rates, equity gaps. Success hinges on IP (Neuracle’s decoding patents) and moats against copycats. By 2040, augmentation markets (memory enhancement) could dwarf medical at $100B+, but ethics boards will gatekeep.

Future U.S. China Rivalry Outlook

Expect cross pollination: U.S. AI algorithms + China hardware. Peng’s vision brain AI “high bandwidth” bridges positions BCIs as silicon carbon fusion. U.S. strengths in software could counter China’s scale; watch for JVs or talent flows amid export controls.

Check out more on our blog page now → AI, Tech, Cybersecurity