Generative AI exploded in 2024 and 2025, birthing a startup every minute. But now, reality is hitting hard. Two popular models LLM wrappers and AI aggregators are flashing warning signs. Darren Mowry, Google’s VP leading startups across Cloud, DeepMind, and Alphabet, calls this their “check engine light” moment. With AI funding dipping 20% in Q4 2025 per CB Insights, thin ideas won’t cut it anymore.

What Are LLM Wrappers?

These startups take powerhouse models like Claude, GPT, or Gemini and add a simple user interface or product layer to tackle niche problems. Think of an app using AI to quiz students or summarize notes. But Mowry warns: if you’re just white labeling these models with minimal tweaks, investors and users are losing patience.

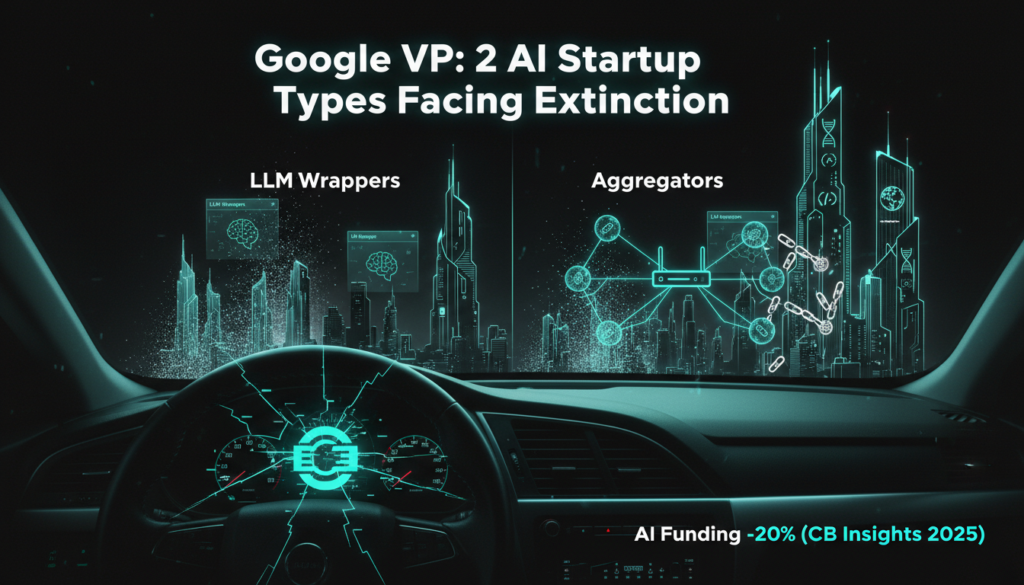

“Wrapping thin intellectual property around Gemini or GPT 5 isn’t enough,” Mowry says. You need “deep, wide moats” either broad innovations or laser focused vertical expertise. Successful examples? Cursor, the GPT boosted coding sidekick that’s raised over $100M, or Harvey AI, dominating legal research with custom fine tuning. According to PitchBook data from late 2025, wrappers with proprietary data moats saw 3x higher survival rates than basic ones.

Back in mid 2024, slapping a UI on GPT could snag users fast. No more. Model providers like OpenAI and Google are rolling out enterprise tools, forcing startups to deliver real value like specialized training data or seamless integrations. A 2025 McKinsey report notes that 60% of AI startups now prioritize “defensible IP” to avoid commoditization.

AI Aggregators: Stay Away

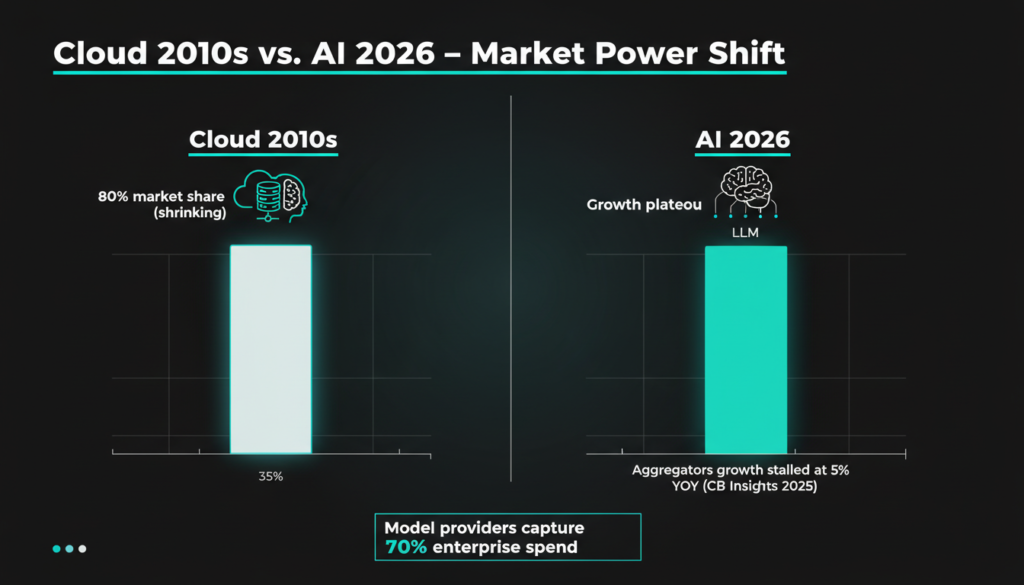

Aggregators are wrappers on steroids. They bundle multiple LLMs into one dashboard or API, routing queries smartly with extras like monitoring or governance. Platforms like Perplexity for AI search or OpenRouter for devs fit here. They’ve grabbed market share, but Mowry’s advice to newbies is blunt: “Stay out.”

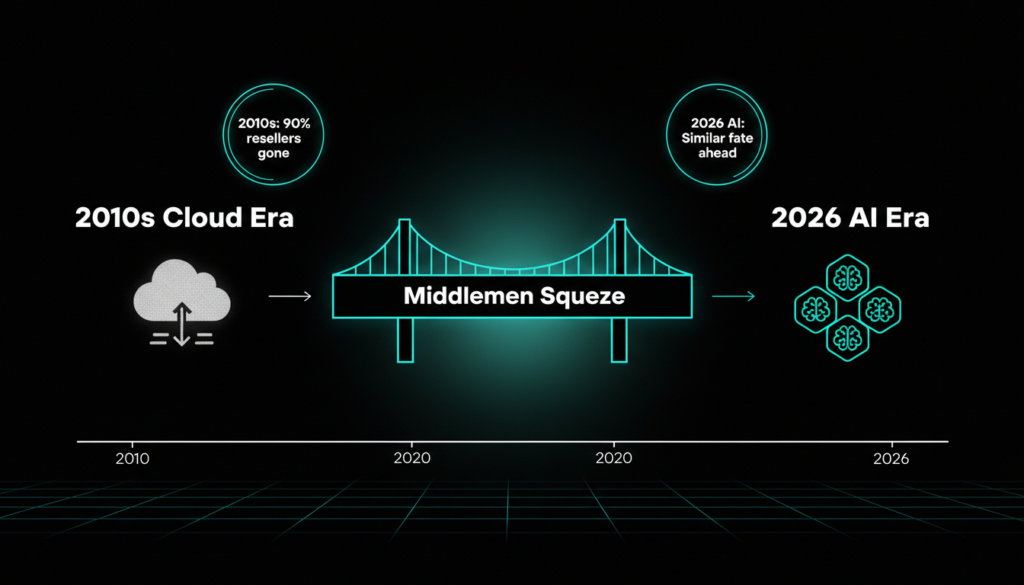

Why? Users crave smarts baked in routing based on query needs, not just cheap compute. Aggregators face razor thin margins as big players add their own multi-model features. Mowry draws parallels to the 2000s cloud boom: AWS resellers popped up for easy access, billing, and support. Most died when Amazon built direct enterprise tools. Survivors? Those adding security or DevOps magic.

Today’s squeeze is real. Google Cloud’s 2025 startup report shows aggregators’ revenue per user dropping 15% amid provider expansions. A Forrester analysis predicts 40% of aggregators will consolidate by 2027, squeezed by native APIs from Anthropic and xAI.

Cloud Lessons for AI Survival

Mowry knows clouds inside out from AWS and Microsoft stints to Google. The pattern repeats: middlemen thrive only with unique services. AI’s next? Expect model giants to dominate enterprise, sidelining pure aggregators. But opportunities abound elsewhere.

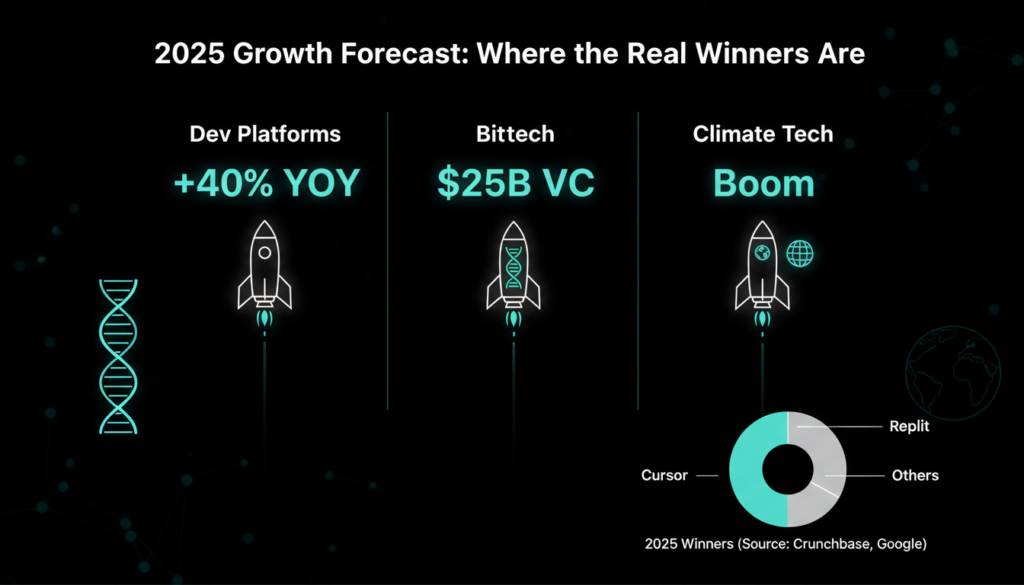

Winning Bets: Dev Tools and Beyond

Mowry’s optimistic on “vibe coding” platforms dev tools exploding in 2025. Replit, Lovable, and Cursor (all Google Cloud fans) pulled massive funding and users. Direct to consumer AI shines too: imagine film students using Google’s Veo to animate scripts affordably.

Broader wins? Biotech and climate tech. VC poured $25B into biotech in 2025 (per Crunchbase), fueled by AI crunching massive datasets for drug discovery. Climate startups leverage satellite data for carbon tracking unthinkable pre AI. Google’s 2026 startup forecast predicts 40% growth here, blending AI with real world data moats.

Build moats with proprietary data or vertical expertise like cybersecurity for enterprises or specialized creative tools and you’ll thrive in this shakeout.

Key Takeaways & Future Outlook

To wrap up Mowry’s insights, here are actionable points for founders navigating 2026’s AI landscape:

- Moats Matter Most: Per a16z’s Q1 2026 AI report, startups with “data moats” (e.g., proprietary datasets) raised 4x more capital than UI only wrappers. Focus on verticals like healthcare (e.g., PathAI’s pathology AI) or finance (e.g., Upstart’s lending models).

- Funding Shifts: Bessemer Venture Partners’ 2026 State of the Cloud notes AI infra deals dominated (e.g., $500M+ rounds for chipmakers like Grok’s xAI), while app layer startups need proven traction. Total US AI VC hit $50B in 2025 but expects a “quality over quantity” pivot.

- Enterprise Playbook: Google DeepMind’s recent Vertex AI updates include built in multi LLM routing, eroding aggregator value. Winners integrate with ecosystems think Cursor’s VS Code plugin hitting 1M users.

- Hot Sectors Deep Dive: Biotech AI funding surged due to tools like AlphaFold 3 (DeepMind’s protein predictor), accelerating trials by 30% (Nature 2025 study). Climate tech? Startups like Pachama use AI for forest carbon credits, securing $100M+ from Breakthrough Energy Ventures.

- Risks Ahead: Watch compute costs NVIDIA’s Blackwell chips drove 2025 margins down 25% for heavy users (Gartner). Regs like the EU AI Act’s US ripple effects demand governance from day one.

Check out more on our blog page now → AI, Tech, Cybersecurity